Writing a check takes less than two minutes but if you’ve never done it before, the blank fields can feel surprisingly confusing. If you’re a renter who just got their first apartment, a college student paying tuition, or anyone in a world of Venmo and Zelle who suddenly needs a paper payment, this guide shows you exactly how to write a check correctly, step by step.

We’ll cover every field on the check, work through examples for the most common dollar amounts (including $250, $1,500, and $2,000), explain how to handle cents and zero cents and answer the most common security questions people have about their routing and account numbers. If you’re searching for how to write a check without making mistakes, this guide keeps the process simple and easy to follow.

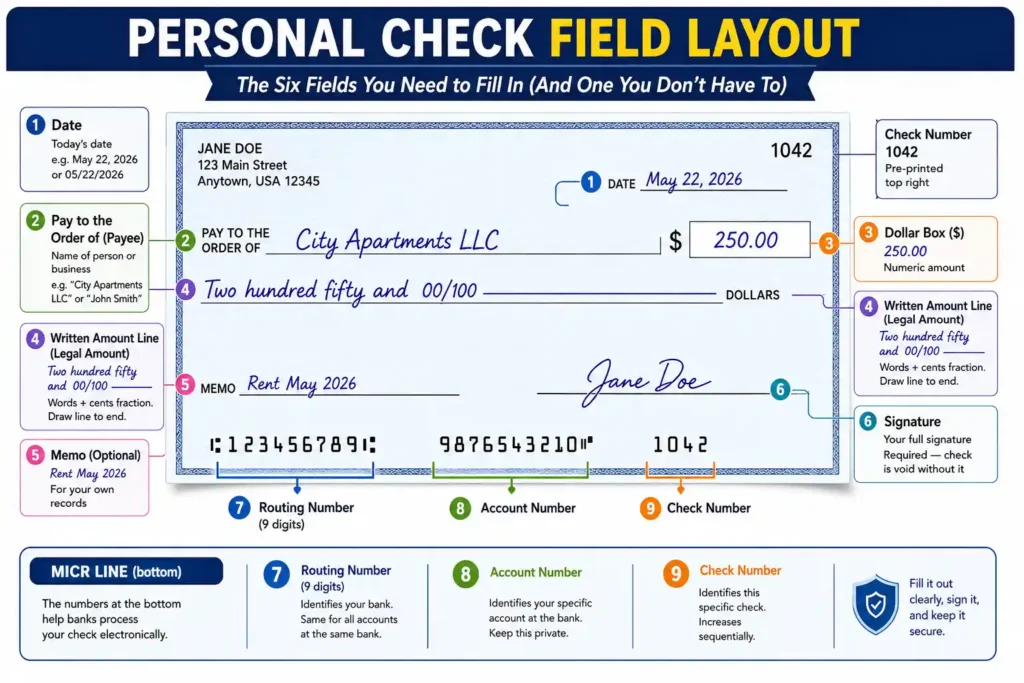

What Every Field on a Check Actually Means

A personal check has six key fields: the date, the payee name (“Pay to the Order of”), the numeric dollar amount box, the written dollar amount line, the memo line, and your signature. The bottom of the check contains your routing number, account number, and check number printed in magnetic ink (MICR line) for bank processing.

Think of a check as a formal, written instruction to your bank: “Pay this person this exact amount from my account.” Every field exists for a reason legal clarity, fraud prevention, or bank processing.

The Six Fields You Need to Fill In (And One You Don’t Have To)

Here’s a visual of what a standard personal check looks like with all fields labeled:

The Numbers at the Bottom: Routing vs. Account Number Explained

The numbers printed along the bottom of your check in that distinctive monospace font are processed using MICR (Magnetic Ink Character Recognition) a technology adopted by the U.S. banking system in the 1950s and standardized by the Federal Reserve for automated check clearing.

Routing Number (9 digits): Identifies your bank. Every branch of the same bank shares the same routing number. This is semi-public it’s printed on every check you write.

Account Number: Identifies your specific account at that bank. This is sensitive and should never be shared carelessly.

Check Number: The sequential number of that specific check in your checkbook.

How to Write a Check: 6 Simple Steps in the Right Order

To write a check: fill in today’s date, write the payee’s full name, enter the dollar amount in the small box, write the same amount in words on the line below (with cents expressed as a fraction over 100), add an optional note in the memo line, and sign your name. Always draw a line to fill the blank space after the written amount.

Follow these steps in order skipping one or doing them out of sequence is a common cause of mistakes when learning how to write a check for the first time.

Write Today’s Date (Top Right)

Use the full date month, day, and year. Either “May 22, 2026” or “05/22/2026” is acceptable. You can post-date a check (write a future date) if you and the payee agree the check won’t be deposited until then though legally, your bank is not required to honor the post-date.

Write the Payee’s Name After “Pay to the Order of”

This is the person or business you’re paying. Write their full legal name or the exact name of their business. Spelling matters if the name doesn’t match their bank records, the check may be rejected or create delays.

Enter the Dollar Amount in the Small Box ($)

Write the number clearly, starting from the far left of the box to leave no room for alterations.

For example: 250.00 Or 1,500.00 . Always include the cents, even if they’re zero. This is one of the most important parts of how to write a check safely and accurately.

Write the Amount in Words on the Long Line (The Legal Amount)

This is the most important field. Under the Uniform Commercial Code, this written line is legally controlling if your handwritten words say a different amount than the numeric box, the words win. Write the dollar amount in full, then express cents as a fraction over 100. Example: “Two hundred fifty and 50/100.” Draw a horizontal line to fill any remaining blank space.

Add a Note in the Memo Line (Optional)

The memo line is for your own reference “Rent May 2026,” “Invoice #4821,” or “Birthday gift.” It has no legal effect but is extremely useful for your records and for the payee to identify the payment.

Sign Your Name on the Signature Line

Use the same signature associated with your bank account. A check without a signature is completely invalid it will be returned unpaid. Never sign a blank check in advance.

How to Write a Check for Any Dollar Amount With Examples

Write the dollar amount in words starting with the largest unit (thousands, hundreds, then tens/ones), followed by “and” and then the cent amount expressed as a fraction over 100. For zero cents, write “and 00/100.” For $1,500: write “One thousand five hundred and 00/100.” Always draw a line through the remaining blank space.

Writing the check amount in words is the part that trips up most people especially the cents format and large numbers. Here’s everything broken down clearly for anyone learning how to write a check correctly.

How to Write Cents on a Check (Including Zero Cents)

Cents are always written as a fraction out of 100, not as a decimal. This applies whether you have 50 cents, 25 cents, or no cents at all.

The Rule: Cents = [number of cents] / 100. So 50 cents = 50/100. Zero cents = 00/100. Never write “.50” or “fifty cents” the fraction form is the accepted standard on personal checks.

For checks with zero cents, you have two valid options: “and 00/100” or “and no/100”. Both are accepted by U.S. banks. However, “00/100” is the most universally recognized and unambiguous format use it to be safe.

Quick Reference: Common Check Amounts Written Out in Full

Save or bookmark this table these are the most searched check amounts and exactly how to write them on the written amount line:

| Dollar Amount | Written on Check (Amount Line) | Notes |

| $250.00 | Two hundred fifty and 00/100 | No “and” before “fifty” |

| $250.50 | Two hundred fifty and 50/100 | 50 cents as fraction |

| $500.00 | Five hundred and 00/100 | |

| $1,000.00 | One thousand and 00/100 | |

| $1,500.00 | One thousand five hundred and 00/100 | “And” only before cents |

| $2,000.00 | Two thousand and 00/100 | |

| $2,500.75 | Two thousand five hundred and 75/100 | |

| $5,000.00 | Five thousand and 00/100 |

Common Mistake: Many people write “and” between hundreds and tens for example, “Two hundred and fifty.” In standard U.S. check writing, “and” is reserved exclusively to separate dollars from cents. “Two hundred fifty and 00/100” is correct. “Two hundred and fifty and 00/100” is not it’s ambiguous.

Made a Mistake on Your Check? Here’s Exactly What to Do

If you make a small, minor error, you can sometimes cross it out, write the correction above it, and initial the change but this depends on your bank’s policy. For most errors, the safest option is to write “VOID” clearly across the entire check and start fresh with a new one. Never use correction fluid (white-out) on a check.

When to Void a Check vs. When a Simple Correction Works

Banks vary in their policies on alterations. As a general rule:

- Minor payee name typo: Cross out, correct, and initial most banks will accept this.

- Wrong dollar amount: Void the check. A corrected dollar amount looks suspicious and may be rejected.

- Wrong date: Cross out, rewrite, and initial generally acceptable.

- Used correction fluid: Automatically void. Banks treat white-out as a red flag for fraud.

Never use white-out on a check. Correction fluid is a known tool of check fraud and will cause the check to be rejected and may trigger a fraud investigation with your bank.

How to Write “VOID” on a Check the Right Way

To void a check, write the word VOID in large, clear capital letters across the front of the check covering the payee line, the amount box, and the signature line. Use a black or blue pen. This makes the check non-negotiable (it cannot be cashed or deposited).

Keep voided checks in your records they’re commonly requested when setting up direct deposit or ACH bank transfers, because they provide your routing number and account number in a verified format.

Check Safety 101: What Your Routing Number Can (and Can’t) Reveal

Your routing number alone poses minimal risk it’s essentially your bank’s public identifier, visible on every check you write. However, sharing both your routing number and account number together is genuinely risky, as this combination can be used to set up unauthorized ACH (electronic) payments from your account. Never provide both to unverified parties.

Routing Number vs. Account Number: Which One Is the Real Risk?

This is one of the most common concerns for check writers especially after you hand a check to someone you don’t fully know, like a new landlord or a contractor.

| Information | What It Identifies | Risk Level If Shared Alone |

| Routing Number | Your bank (e.g., Chase, Wells Fargo) | Low semi-public, identifies bank only |

| Account Number | Your specific bank account | Medium combined with routing number, creates risk |

| Both Together | Full payment credentials | High enables ACH payments from your account |

| Signature Sample | Your authorization mark | Medium could enable forged checks if combined with account info |

If you believe someone has both your routing and account numbers without your authorization, contact your bank immediately. Under FDIC guidelines, you can request a new account number to protect your funds. Acting quickly is essential the faster you report, the more protections apply under the Electronic Fund Transfer Act.

What Is the $3,000 Rule in Banking? (Simply Explained)

This question appears constantly in check-related searches, so let’s clear it up directly.

Under the Bank Secrecy Act, banks are required to keep records of cash purchases of monetary instruments like money orders or cashier’s checks between $3,000 and $10,000. This is a record-keeping requirement, not a public reporting requirement.

The $3,000 rule (record-keeping) and the $10,000 rule (reporting) are two different things. At $10,000+, the bank must file a Currency Transaction Report (CTR) with FinCEN. Below that, they only need to log it internally. Neither rule applies to personal checks between private individuals.

The rule most people are actually worried about is structuring deliberately breaking up cash transactions into smaller amounts to stay under the $10,000 reporting threshold. That is illegal under the Bank Secrecy Act regardless of whether the money itself is legitimate.

Conclusion

Now that you know exactly how to write a check from filling in each field in the right order to writing dollar amounts in words and understanding what your routing number means the whole process should feel completely manageable every time you pick up a pen. The most important thing to remember: the written amount line is the legal one. Write it carefully, extend a line through the blank space after it, and sign clearly. That combination makes your check valid, tamper-resistant, and bank-ready.

Whether you’re paying rent, sending a gift, or handling a business payment, knowing how to write a check properly is still an important financial skill. Once you understand how to write a check step by step, the process becomes quick, secure, and easy to repeat anytime you need it.